Context

Insurance has always worked the same way. Something bad happens, you file a claim, someone comes to assess what you lost, and eventually you get paid. The model is slow, expensive, and often disputed. Over the last two decades, a different model has emerged: parametric insurance. Instead of paying based on what an assessor verifies, it pays based on what a measurement says – if the measurement crosses an agreed threshold, then the payout is automatic.

Take this example: In October 2025, the Government of Mozambique received $5.4 million to deal with the aftermath of a drought and a tropical cyclone. The money was paid out in days, not months. Nobody from an insurance company visited the country to verify what had happened. Satellites had measured how much rain had fallen and how the crops were doing, the numbers came in worse than the agreed limits, and the payment was triggered automatically.

The payment came from the African Risk Capacity (ARC), a disaster insurance pool that 35 African governments have set up together. ARC has been doing this for African governments since 2014, and the Caribbean Catastrophe Risk Insurance Facility (CCRIF) has been doing the same for Caribbean countries since 2007.

But this model is expanding fast. What started as a tool for governments and farmers is now being used to protect and insure a plethora of assets: a solar farm against weak sunshine, a port against shutdown from cyclones, a forest against wildfire, a coastal home against flooding, a mine against pit closures from heavy rain, a fish farm against marine heatwaves. Major reinsurers and a new generation of parametric specialists write these products, and a growing fleet of public and commercial satellites supplies the data. Underneath the expansion is one structural shift: parametric insurance is becoming increasingly viable for risks that used to be uninsurable, because EO can now see things it couldn't before.

Earth Observation and Parametric Insurance

EO is the engine of parametric insurance: every time a satellite gains the ability to measure a new variable at a new resolution at a new frequency, a category of risk becomes parametrically insurable. Soil moisture, vegetation health, flood extent, fire severity or sea surface temperature are a trigger for an insurance policy somewhere in the world, because some satellite(s) is measuring it.

Before satellites, parametric had to mainly rely on ground-based weather stations such as rainfall gauges, thermometers, wind sensors at fixed locations which limited the market to a handful of perils in places where stations happened to be dense enough. In other words, without EO, parametric was a small market built around weather stations, while with a growing number of EO satellites, parametric is now a fast-growing market.

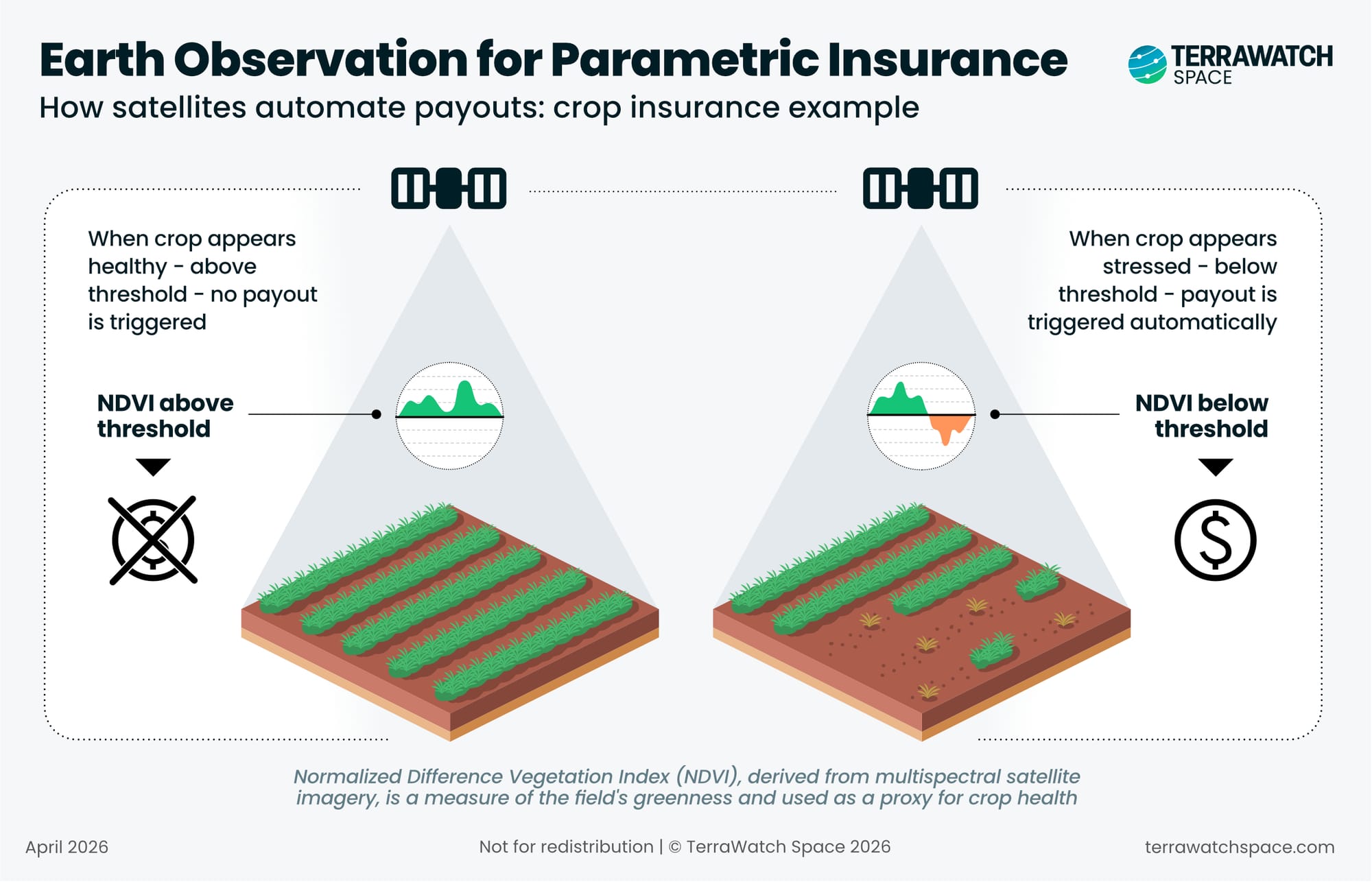

The visual below illustrates, in a simplified manner, how this works in practice. A satellite measures the crop's health over the growing season. If the crop is healthy, nothing happens. If the crop seems stressed beyond an agreed threshold, the policy pays out automatically, without anyone visiting the field (more on the actual mechanics later).

The rest of this piece walks through where the market is, who is building it, and where it is going. This essay is organised into seven sections:

- How Parametric Insurance Works

- The Four Components of Parametric Insurance

- Understanding Parametric Insurance: A Wildfire Risk Example

- Why Earth Observation Matters

- From Soil Moisture to Flood to Renewables

- The Parametric Insurance Landscape

- Agriculture, Public Sector, Infrastructure and So On

- The Parametric Insurance Stack

- Public EO Missions

- Commercial Satellite Companies

- Insurers, Reinsurers, and Parametric MGAs

- Basis Risk: The Limits of Parametric Insurance

- A Real-Life Case Study of Basis Risk

- Mitigating Strategies: The Role of EO

- Outlook for EO and Parametric Insurance

- Trends and Constraints

- Closing Note