Edited on 10 May to include Privateer’s acquisition of Orbital Insight.

To the paid subscribers, thank you for your support - it allows me to write these deep dives while letting me continue to offer the weekly newsletter for free. The next deep dive will be EO for Wildfire Monitoring, to be published in the first week of June.

To the free subscribers, this is a short preview of the piece. If you would like to read the full deep dive, please upgrade your subscription.

The last few months have seen some interesting developments in the usually quiet corner of the EO sector: Platforms.

EO space situational awareness firm Privateer Space pivoted and bought major EO platform player Orbital Insight, another recently acquired EO platform provider Descartes Labs acquired a niche platform Geosite, an EO platform for the insurance sector and Planet launched its Insights Platform following the acquisition of Sinergise (Sentinel Hub).

We also saw startups like Danti, an EO data search engine and Fused, a serverless EO processing and visualisation platform raise funding and others like Astraea getting acquired by Nuview, an EO satellite startup. And there is more to come. So, this may be a pretty good time to look at the state of EO platforms, what has happened so far and where we are going.

Preamble

If you have been following the Earth observation sector, you should have heard of platforms. It is one of those long-lasting buzzwords that will continue to be the next big thing for a while. Why? Because I don’t think anybody has cracked the puzzle with EO platforms. Very few care about this corner of the EO sector - roughly 7 out of 10 people care about EO satellites, and 3 out of 10 people seem to care about EO applications, which means no one actually cares about EO platforms. And, as any consultant should, I have got some data to prove my point.

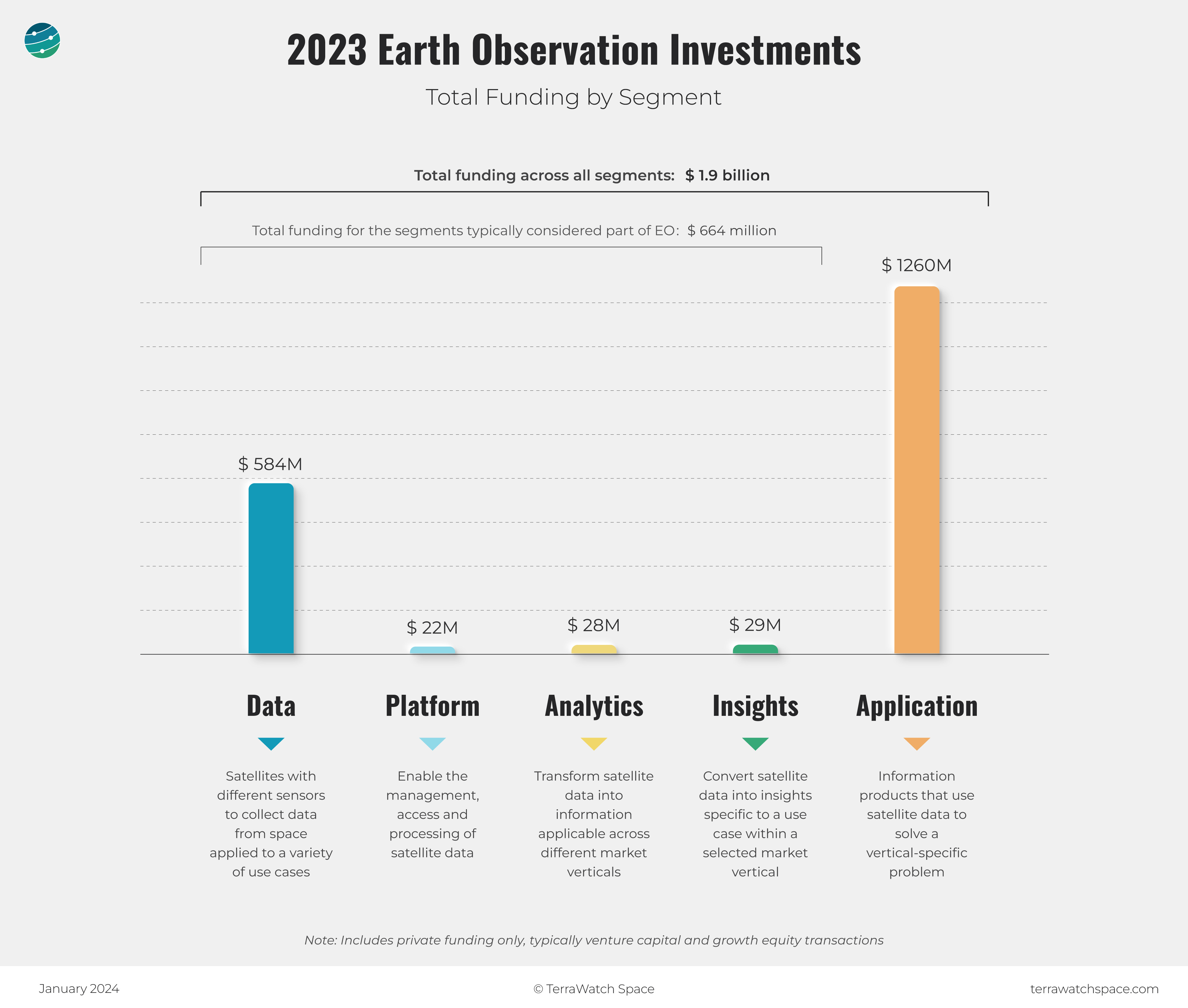

Here is a summary of total EO funding in 2023 (the numbers for 2022 are also not very different). This somewhat resembles the smiling curve1, according to which the upstream and downstream segments provide more value-added to a sector compared to the intermediary segment.

This is not surprising - platforms are abstract. They do not represent the raw materials nor do they represent the final product. They are the building blocks in the middle that help make that translation process happen, not for one, but for many at the same time. If you have read my stuff for a while, you know my overarching thesis of EO:

Earth observation is a sector that is built by tens of thousands of people and used by hundreds of millions of people. And, for the sector to grow, we need to make it easy for the former to explore and innovate with EO so that they can solve the problems of the latter.

As the figure above shows, we are seeing rapid growth in the emergence of companies in the ‘Insights’ and ‘Applications’ segments. I am convinced that the only way to enable more users to derive value from EO in a way that is efficient, scalable and reliable is to give them the power to do so.

As the figure above - extracted from the TerraWatch 2023 EO Investments analysis - shows, the intermediary Platform and Analytics segments received less than 3 percent of overall funding in the year. That figure was slightly higher at 5 percent for the 2022 investments. Note that this figure may not include the investments in platforms made by companies in the Data segment like Planet, Maxar and Pixxel among others, which have their in-house platform initiatives.

However, in terms of exits, Platforms might be the most happening segment of the EO market. Just in the last couple of years, we have had Privateer Space acquire Orbital Insight Descartes Labs sold to Antarctica Capital, Sinergise bought by Planet, Astraea acquired by Nuview and Geosite integrated/strategically acquired by Descartes Labs. Four Five exits in two years- not so bad, eh? But, why is Platforms the most overlooked segment in the EO market?

In this piece, we will dive deep into the EO platform layer starting with why we need EO platforms in the first place, the market segments within EO platforms, the commercial landscape, why EO platforms have failed to take off so far and the way forward for this segment. Note that while a portion of the piece is a market analysis (and hence factual), the other half of the piece is an opinion (and hence subjective). All comments and feedback are welcome!

Here is what we have in store:

- EO Platforms: Market Segments

- EO Platforms: Commercial Landscape

- Why Commercial EO Platforms Haven’t Taken Off

- Outlook

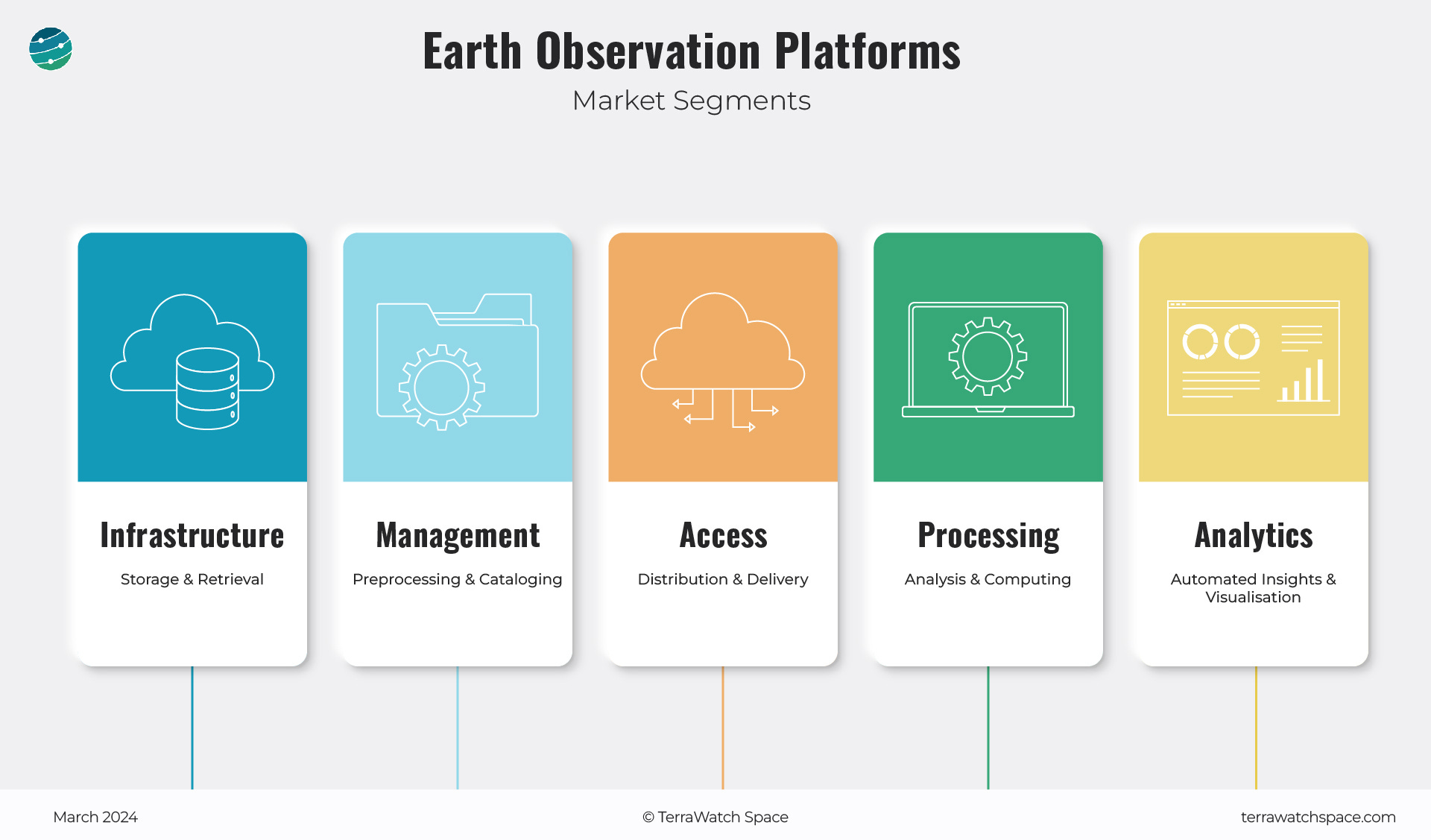

EO Platforms: Market Segments

Context: The Role of Platforms

EO platforms are generally needed to perform three major functions in the EO sector: accessibility, usability and fusability.

- Accessibility: To enable users to find EO data and potentially, analytics that are not only transparently priced and affordable, but also remove the pain (licensing and distribution), associated with the process of acquiring EO data;

- Usability: To make sure data that is available for access is usable or comes with tools to make it usable (in whatever form that is ideal for a user),

- Fusability: To facilitate the fusion and processing of data from various sources, to convert raw data into useful intelligence, through what could essentially be a sensor-agnostic, data-agnostic, compute engine for EO.

The foundational layer that powers all three functions would be the underlying infrastructure, typically the cloud, that enables the end-to-end process of translating raw data into useful intelligence.

The Five Segments of EO Platforms

Considering the roles of platforms described above, I classify the EO platform segment into five market segments. The motivation for doing this is simply to go beyond the buzzword of ‘platforms’ and try to understand what platforms bring to the EO sector and the important boring problems2 they are involved in solving.