Written by Filip Kocian (ex-investor at Expansion Ventures, now a space-industry analyst), who wore the finance hat and Aravind Ravichandran (founder and CEO of TerraWatch Space, an independent research and advisory firm), who wore the strategy hat.

We have tried to make this accessible even if you don't come from finance. It is in three parts – what Advent bought, what Vantor's becoming, and what the exit requires. So you can read straight through or jump to what interests you.

Lastly, this is industry analysis, as of May 2026, not investment advice. The views are the authors' own, and we certainly welcome comments.

Just about three years ago, private equity firm Advent International completed its acquisition of Maxar Technologies and took the company private after 14 years of trading as a premier listed Earth observation (EO) company.

Private equity (PE) firms are no strangers to the space sector, especially on the industrial side of aerospace and defense. Both generalist firms (such as KKR and Blackstone) and sector specialists like AE Industrial Partners illustrate how private equity operates in the space industry.

Still, the Maxar buyout might be a standout example. It is quite an important company in the EO/geospatial and the wider space industry as well as an intelligence supplier to the US government. At the time of the acquisition, Maxar produced more geospatial revenue than all of its newer competitors combined. Further, this gives a window into the PE playbook applied to a hardware-heavy player with a concentrated customer base.

PE firms hold companies for six years on average. So, at this natural midpoint, we wanted to analyze Advent’s acquisition of Maxar (now rebranded to Vantor), developments at the company so far and the roadmap forward. Advent's $6.4 billion Vantor bet is neither a financial engineering play nor a hardware story, but rather what looks like a forced software transformation whose exit math depends on a multiple expansion that the current customer concentration may not allow.

Part I — What Advent Bought

1. Maxar Was in Worse Shape Than the Price Suggested

Recapping the acquisition structure, acquirers paid $6.4 billion to take the company private – breaking down into a $2.3 billion debt facility from Sixth Street Partners, $3.1 billion equity component from Advent alongside a smaller $1 billion equity co-investment from Canada’s British Columbia Investment Management.

Under the fairly high headline figure is a much more difficult snapshot of a company that was overleveraged and with declining revenues.

For 2022, the last full year as a listed company, Maxar revenues dropped 9.3% from $1.77 billion to $1.6 billion. Even worse, the company's operating income – how much the business generates from regular operations before taxes and financing costs – fell 94% to just $11 million. This stood in stark contrast to Maxar's leverage. The company carried ~$2.2 billion of debt, generating $158 million in interest expense in 2022 against just $11 million of operating income. In other words, operations came nowhere near covering the interest burden, and the resulting deficits ate into cash reserves while the balance of notes to repay kept growing.

The difficult position of Maxar had three major sources:

- Decline of the geostationary communications satellite orders. Before the acquisition, manufacturing of satellites for commercial satellite operators was a second major business for the company outside of Earth Observation. From as early as 2018, uncertainty about the geostationary communication satellite business prospects would hit Maxar’s lucrative satellite manufacturing business.

- Satellite failures. Maxar suffered major complications with satellites in orbit. In the case of WorldView-4 (which failed in orbit in 2019), it meant a small insurance payout in contrast to expected revenue of the ~$200 million per year order of magnitude. Failure of satellites built for customers like the case of SXM-7 (for SiriusXM) mainly impacted its reputation and thus future orders. Equally, manufacturing problems and supply chain issues affected satellites in production on the ground like Ovzon-3 or Jupiter-3 satellites from EchoStar. In practice that meant that rather than customers paying for delivering its satellites, Maxar was forced to pay them not to cancel those contracts over production delays.

- Legion. Maxar's next-generation WorldView imaging satellites were announced in early 2017 but were still on the ground at the point of the PE acquisition. The first pair didn't launch until May 2024 (seven years after announcement) with the constellation completed in February 2025. At acquisition, that meant ~$800 million of assets under construction with no revenue yet to show for it.

Advent acquired the company for $6.4 billion, a hefty price tag for the distressed company at the time but a modest premium of 34% compared to its more reasonable 52-week high. Given Advent's refinancing of this debt amid a difficult post-COVID credit environment, we anticipate roughly $220 million [1] in annual debt service following the acquisition, above the ~$158 million Maxar carried pre-deal, reflecting both the larger facility and higher post-COVID rates.

When the deal was announced, there were two apparent levers for value creation:

- Launching Legion. Getting Legion to launch would untangle $800 million in balance sheet burden into a productive asset and allow it to service some of the related debt load.

- Multiple arbitrage. The bleeding satellite manufacturing division was apparently constraining Maxar’s overall multiple. Separating a relatively healthy Earth Intelligence business could see that business valued at multiples closer to software or tech companies and less like a depressed hardware manufacturer.

2. The Divestments Didn't Move the Needle

Set Maxar aside for a moment. Advent has run this playbook before. In 2020 it took the British defense conglomerate Cobham private for $5 billion, then broke it apart: Cobham Mission Systems to Eaton for $2.85 billion, CAES Defense to Honeywell for $1.9 billion, CAES Space to Veritas Capital for a reported ~$2 billion, and Cobham Aerospace Communications to Thales for $1.1 billion, alongside smaller units like Cobham Aviation Services. By 2024, Advent had divested more than $6 billion out of a ~$5 billion purchase and it had recovered more than it paid before even valuing what remained.

At Maxar, the same playbook structurally did not work. The divestments have been small and few: WeatherDesk, sold to the Finnish weather company Vaisala for $70 million, and the radio-frequency monitoring assets from Maxar's earlier Aurora Insight acquisition, for what we assume was immaterial consideration.

The divestment that mattered was the big one. Advent split Maxar's two divisions immediately after taking control – Earth Intelligence becoming Vantor, satellite manufacturing becoming Lanteris Space Systems. Then, about two and a half years later, Intuitive Machines (LUNR) bought Lanteris for $800 million: $450 million in cash and $350 million in LUNR stock, leaving Advent with an undisclosed minority stake (in the mid-teens percent) in a still-unprofitable space company. Taking part of the consideration in stock rather than cash is itself telling as it lets Advent retain upside in the combined entity, a bet that a vertically integrated space prime is worth more than the cash today. It likely also reflects that LUNR, still unprofitable, could not have funded an all-cash deal [2]. The stock has appreciated meaningfully since.

The price is worth dwelling on. At roughly 1.3x revenue ($800 million against Lanteris's ~$600 million of 2025 revenue), it sold well below its satellite-manufacturing peers such as York Space (~10x), Rocket Lab (~60x), even Terran Orbital at acquisition (~5x), and did so despite being one of the few in that group with positive EBITDA rather than losses. Part of the discount reflects Lanteris's own role as the drag that suppressed Maxar's multiple in the first place. The larger explanations are structural: limited growth and backlog expectations in its segment, and a constrained buyer universe, with Intuitive Machines a non-traditional buyer for an asset like this. The alternative reading that Vantor quietly received offsetting value elsewhere, such as discounted satellites would normally have surfaced in the disclosures, and didn't.

The secondary benefits are real even so. The $450 million in cash alone covers roughly two years of debt service, or could fund a leverage reduction. The manufacturing cost base, including the operating expenses that had ballooned before the acquisition, now sits with the buyer rather than with Vantor.

The Number Advent Has to Hit

Before we go further, it helps to recap how the returns work. A typical buyout has two layers:

- Debt, usually from banks, funds part of the purchase; it earns only interest, so its upside is capped, but it is repaid first if things go wrong.

- Equity sits behind the debt in priority but captures the upside if the deal succeeds.

Applied to Vantor – The $2.3 billion of debt is repaid first, at par; the $4.1 billion of equity is where the return has to come from. A good PE outcome runs 20-25% a year (measured as IRR) over a roughly six-year hold – so compounding $4.1 billion at ~20% for six years (a ~3x multiple) and adding the debt back at par points to an exit target of around $14.5 billion to clear an attractive return.

$14.5 billion: That is the number that matters, and three divestments later Advent is no closer to it. The break-up playbook that more than paid for Cobham recovered only modest proceeds here, because Maxar's value sat in one business that cannot be carved up, and financial engineering won't bridge the gap either. Which leaves the only lever that can: whether Vantor itself can be made more valuable, through better hardware, productization, and an AI repositioning.

Part II — What Vantor Is Becoming

3. The Space System: From Legion to Vantage

“Vantor represents a company transformed” said Vantor’s CEO Dan Smoot during the Maxar to Vantor rebrand announcement. It has certainly been a busy period for the company, outside of the Lanteris divestment, it has also made changes across hardware-driven imaging capacity, product, positioning, partnerships and revenue structure.

The rebranding choice is one to pause upon as well. Established in 2017, Maxar’s brand became synonymous with high resolution optical satellite imaging. It stood in the upper right corners of viral images capturing a Russian military convoy advancing in Ukraine and of the Ever Given container ship stuck in the Suez Canal. By all means, this was a brand with real equity, and Advent chose to trade it for a claim on an spatial intelligence platform and AI positioning – and the higher multiple that comes with it.

Legion: Finally Flying

Vantor remains ultimately a satellite imaging company and the first good news post-takeover came on that front. The six WorldView Legion satellites, which were delayed for a while, have now been launched and are reportedly working very well. Two more (Legion 7-8) are due in 2027 — a commitment Advent made back in April 2023 to add capacity in response to demand, not a late reaction to how the first six are performing.

Comparatively, Legion satellites are quite similar to WorldView-3 satellite in terms of resolution and imaging capacity per satellite but offer clear advantage as a constellation - the same highest commercial satellite data quality is now available at constellation scale, with corresponding improvements in coverage and latency.

Operational improvements on the constellation are also notable, WV Legion satellites are ~3x lighter and significantly cheaper than a single Worldview satellite. So far, they seem to be operating very well in orbit. Previous Maxar/Vantor satellites have continued to operate in orbit long past their useful life.

The bull case is clear: Legion fleet approximately doubles the overall imaging capacity of Vantor and drastically improves service across two key variables that its most important users value – latency and collection capacity at the highest resolution in the areas of high demand. There is however a looming threat over this proposition where Vantor’s revenue has been historically concentrated toward the US government. Principally the US National Reconnaissance Office buys Vantor's imagery directly, plus allied governments via prime intermediaries. It is not obvious that buyers will absorb Legion's doubled capacity at anything like the rate the exit math needs. In the unlikely worst case, Vantor ends up with the best commercial imaging system on orbit and no incremental buyer for it.

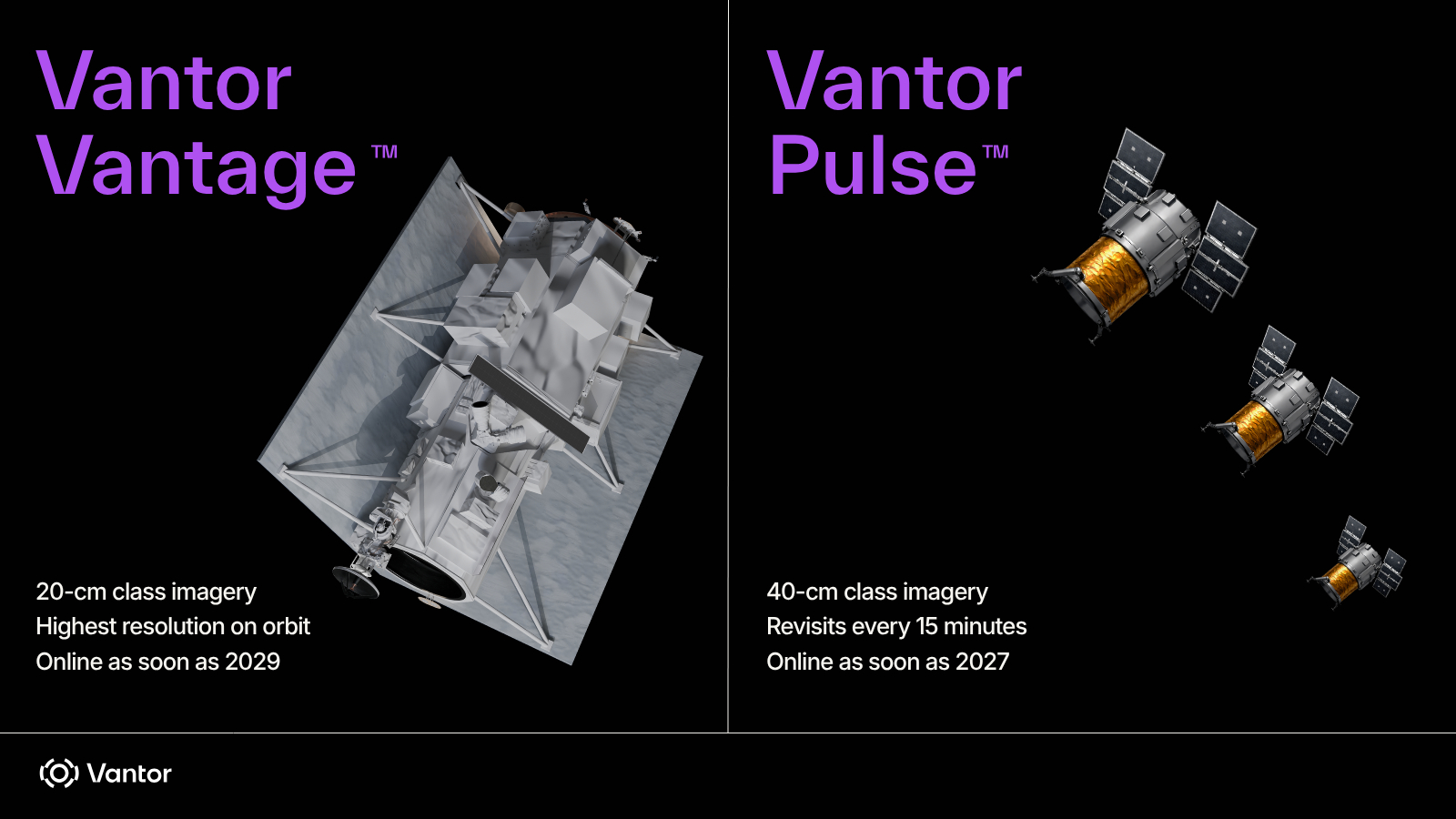

Vantage and Pulse: The New Architecture Bet

On the hardware side, this is the most important announcement Vantor has made in a decade and the first new satellite architecture it has unveiled since Legion itself. Two systems are being built:

- Pulse: A fleet of at least two dozen small satellites at 40 cm resolution, built for a major step-up in coverage and frequency (a 15-minute revisit pattern), with the first satellites launching in 2027.

- Vantage: Two satellites offering an impressive 20 cm resolution from sun-synchronous orbit, targeting 2029 launch date.

Think of the two as designed to work as one, not as separate bets. Pulse's high-frequency, lower-resolution coverage is the tip-and-cue layer that flags where something has changed, while Vantage's exquisite 20 cm resolution is then directed to look closely. Smoot's framing is explicit when he says that customers today solve the resolution-versus-revisit tradeoff by buying from multiple providers, but Vantor wants to collapse that into a single system delivered inside the customer's own environment. It is the hardware expression of the same platform thesis running through the software stack – own the full intelligence cycle, not just the pixels.

If we unpack the announcement, what does it mean?

Industrially, this could be a significant satellite manufacturing order in a sector where non-SDA revenue is scarce. Some of the potential contenders we have heard are York Space Systems, Rocket Lab and Lanteris (the manufacturing arm that was just sold) with Satellogic a wild card on the Pulse side.

The most important market signal, though, loops back to a 2021 GeoIgnite talk, "Why It Takes a Legion," by Dr. Walter Scott, the founder-technologist who embodies much of the WorldView → DigitalGlobe → Maxar saga. There, Scott argued that Legion wins against Planet's and BlackSky's constellations on product-market fit, adaptability, and capital efficiency, the core claim being that a small number of high-performance systems like Legion would beat proliferated constellations on both cost and value to users.

So why has Vantor now built the proliferated layer it once argued against? The architecture is a hybrid, not a reversal: Vantage continues the exquisite model Scott championed, while Pulse adds the proliferated layer. The more interesting question is what shifted in the five years since to make that layer worth building alongside the exquisite one.

Scott's comparison comes down to total utility to users over total constellation capex – and both sides of that ratio have moved. On capex, Legion's price tag came in higher than the talk implied (the video predated the actual launch by three years). On utility, user needs have tilted toward coverage and low-latency imagery, especially over critical regions, which a proliferated model supplies better. And the capability available from smaller form factors has risen sharply: Vantor has already benefited from a roughly 3x mass reduction between WorldView and Legion at comparable performance, and better payloads and buses may have shifted the calculus underneath.

4. Productization: From Pixels to Platform

For all the attention on the new satellites, the transformation that matters more for the exit has been quieter. The first visible change after the Advent acquisition wasn't the rebrand; it was the slow rewiring of how Vantor sells. Where Maxar Intelligence had primarily monetised pixels, Vantor has moved toward a stack where the satellites are infrastructure and the value sits in the software on top. Smoot's own articulation in early 2026: "We've been quietly investing in our platform and operations to create solutions that provide long-term value. Solutions that people want to subscribe to."

The product taxonomy that has emerged is more deliberate than it first appears.

Vivid is the data foundation – the 2D and 3D global digital twin, covering virtually all of Earth's landmass in 2D and 95% of the highest-interest areas in 3D, built on a 20-plus-year archive of high-resolution imagery including the deepest commercial archive of 30 cm-class data.

Tensorglobe is the software platform that operates on that foundation, handling tasking, fusion, hosting, and user access.

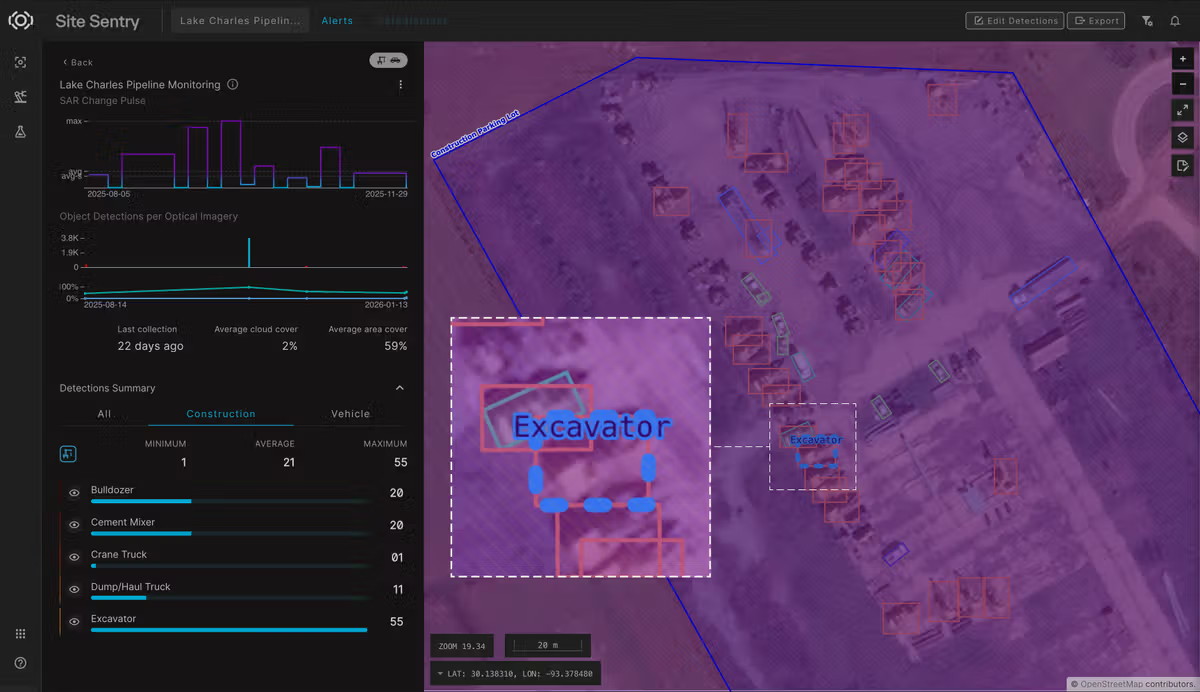

Sentry (persistent monitoring with AI-powered vessel and object fingerprinting) and Raptor (visual positioning for drone navigation in GPS-denied environments) sit on top as mission applications. Think of Vivid as the baselayer, Tensorglobe as the platform that operates on it and Sentry and Raptor as applications on the platform - not adjacent products, but layers of one full stack.

Most EO companies sell satellite output and leave the buyer to integrate it. Vantor sells products that are already integrated into the workflows of the user. The transition from a capability that can be demonstrated to a product that is operationally embedded in the user’s process is where commercial EO adoption typically stalls (a dynamic TerraWatch has covered separately through the Invisibility Curve framework and Use Case definition).

However, Vantor seems to be gradually getting around this with its new evolution as a platform player. For instance, the geospatial intelligence platform that Vantor was awarded a contract for recently will be a customized version of Tensorglobe to be used by 1.2 million government users across 250+ organisations and is embedded in the intelligence community's workflows. Similarly, partnerships with Anduril (combat autonomy) and Windward (maritime monitoring) extend the same pattern into other domains.

The enabling architecture across all of these, beyond the platform layer itself, is actually sensor-agnosticism. Tensorglobe can ingest imagery from any source, Vantor's own satellites and third-party data alike, into one spatial foundation. The 3D imaging capability sits as a particular moat on top of this. Smoot has claimed Vantor is "one of only two companies (alongside Google) with global 3D mapping at scale" – a framing that places the company in tech-platform peer space rather than EO peer space.

5. The Customer Base: The Transition Under the Hood

Across multiple public statements in late 2025 and 2026, Smoot has settled on a consistent claim: 90% of Vantor's revenue is now recurring. The number is consistently cited in his podcast appearance, in his interviews (where he also cited $900M ARR), and in other media, which describes Vantor as "a platform companies depend on, not just buy from."

The anchor beneath all of this is a single contract. In May 2022 the NRO awarded Maxar the Electro-Optical Commercial Layer (EOCL) contract - $3.24 billion over ten years, a $1.5 billion firm five-year base plus $1.74 billion in options through 2032 - the largest commercial imagery acquisition the agency has ever made. EOCL replaced EnhancedView, the contract Maxar (and DigitalGlobe before it) had held for more than two decades. Vantor is anchored to the US government twice over: to the NRO for imagery under the EOCL contract, and to the National Geospatial-Intelligence Agency through the Tensorglobe-based platform it now runs. This, we can argue, is both the foundation of the 90% recurring figure and the concentration risk the exit thesis turns on.

The transition is something Smoot is explicit about attributing to going private. On a podcast appearance, he said: "When you go private, you can actually take the time to reformat the business. Getting the sales motion, getting your customers to buy in a different way is not easy." Another piece gives it a sharper framing: "Wall Street rewards quarterly results. Transformation takes years." This might be one of the cleanest articulations of why the PE structure was a good fit for the then-Maxar – not as financial engineering, but as cover for a multi-year business-model rebuild.

The leadership composition assembled to run that rebuild is another piece of evidence. Smoot arrived from Riverbed Technology where he led the same kind of hardware-to-software transformation under PE ownership. Peter Wilczynski, the Chief Product Officer, spent 12 years at Palantir building its ontology layer and leading the early development of Gaia, Palantir's geospatial mapping product. Susanne Hake, GM of the US Government business, arrived from Palantir as SVP for Strategic Technology Programs, after time at Booz Allen Hamilton. So, two senior Palantir alumni running products and the US government, plus a proper operator as CEO, is not just coincidental casting, but can be considered an actual playbook.

The geopolitical environment, especially rising defense spending across US and allied budgets supports the demand side. But US export restrictions on the sale of high-resolution commercial imagery to allied governments cap the rate at which Vantor can diversify away from USG concentration through international growth — a constraint that does not bind in the same way for European players. Vantor's public examples of sovereign deployments such as the Netherlands MoD, an unnamed South Asian government running a Rapid Access Program and a Middle Eastern customer with an in-country 3D production pipeline all show that the company can extract sovereign-style customer relationships within the current regulatory envelope, but each is heavily bespoke.

6. Partnerships: Defining a New Market Category

The partnerships announced in 2025 and 2026 are easier to read together than separately. In quick succession: Vantor is partnering with defense firm Anduril to provide the spatial intelligence layer of a mixed-reality combat system for the US Army. The company has also partnered with Saab for autonomous drone capabilities in Europe and has developed a joint product with Niantic Spatial pairing Raptor's aerial visual positioning with Niantic's ground-based system for GPS-denied military operations. More recently, Vantor embedded Sentry inside Windward's Maritime AI platform for dark-vessel tracking and also announced plans to deploy Google Earth AI models in classified environments via Tensorglobe.

Read together, the pattern is consistent: in every partnership, Vantor is either the spatial intelligence layer underneath someone else's mission application (Anduril mixed reality, Windward’s maritime platform or Niantic Spatial positioning) or the deployment platform for someone else's AI capabilities into customer environments those providers cannot operate in directly (Google). The strategy is not what you would expect typically with EO companies, which is to build end-applications that compete with vertical AI providers, but rather Vantor is moving towards making itself the indispensable infrastructure layer those vertical providers integrate with.

The partnerships fall into three patterns. Some bring capabilities Vantor cannot build itself, with Google's geospatial AI models being the clearest example. Some are product co-building activities especially for the defense sector such as with Anduril, Saab and Niantic Spatial. And finally, those like Windward bring a new commercial market that Vantor would have found difficult to crack without the domain expertise.

This is basically the Palantir playbook for a different layer of the stack. While Palantir is now the de facto ontology layer for the defense sector, Vantor is positioning itself as the spatial intelligence layer that does the equivalent job for anything operating in physical space. The hires, the platform architecture, the partnership selection, and the rebrand framing all corroborate the same direction. Either Palantir absorbs the spatial layer over time by commodifying Vantor, or Vantor builds enough product surface and customer entanglement that it becomes the layer Palantir has to integrate with rather than replace. The next 18 months will decide which.

One thing to watch: whether the same partnership pattern is also buyer signalling. The Google relationship is structurally the most interesting: Google has the balance sheet to clear the exit math, the strategic logic via Earth AI and Google Maps and a motivation to enter the sovereign-AI deployment business through a partner rather than directly. Whether the Earth AI integration is the early shape of an acquisition discussion or a commercial agreement is not clear as it might be too early.

Taken as a whole, this partnership architecture supports what TerraWatch has previously called the sovereign intelligence stack thesis – Vantor is no longer selling imagery, it is selling an integrated stack where data, models, fusion, and delivery happen inside the customer's secure environment. The architecture remains defense-first and whether commercial follows is the familiar EO question of whether defense demand ever crosses over into commercial scale that TerraWatch has discussed in-depth before.

Part III — What the Exit Requires

7. The Exit is not a Buyer Problem, it is a Multiple Problem

We’ve now seen how the company has fared under the new ownership. Advent’s hands-on strategic thinking on new spacecraft architecture and narrative shift across positioning, product and partnerships was supported by the tailwinds of AI and increased defense spending globally. On a traditional PE timeline, the next three years are when Advent has to convert that value creation into a return on equity, turning "the company transformed" into an actual exit.

Two questions decide whether it reaches the magic ~$14.5 billion figure: how Vantor's performance has developed away from public-market scrutiny, and what the market will pay when it goes out to sell.

Business performance

The $6.4 billion was roughly 4x Maxar's $1.6 billion of 2022 total revenue, while Vantor's Earth Intelligence segment was about $1.08 billion of that. We assume revenue has grown meaningfully from that ~$1.08 billion base as Vantor has launched six high-end satellites, with Legion 7-8, Vantage, and Pulse still to come, and in a capacity-constrained market that is a real opportunity to push the topline up.

The bearish read is on how fast that growth could realistically have come. Several of the products and partnerships are still early – the customer base remains concentrated on the US government and competition has intensified from sovereign systems, commercial constellations, and international providers. And the contract that anchors the base, EOCL, comes up for recompete in roughly the window Advent would be exiting. The firm five-year base runs to about 2027, with options to 2032, so a buyer is underwriting a renewal as much as a run-rate.

The EBITDA picture from old Maxar is harder to read. Earth Intelligence produced ~$445 million of adjusted EBITDA in 2022 which is roughly 14x on the $6.4 billion enterprise value, though that figure was depressed by the Space Systems losses and corporate overhead now stripped out. Even assuming Vantor has since doubled revenue (well beyond its historical trendline) and widened margins, holding the entry multiple still wouldn't clear ~$14.5 billion. The return has to come from the multiple itself expanding.

Multiple expansion

That leaves the whole thesis resting on one thing: the buyer accepting the spatial-intelligence story. The exit only works if a buyer values Vantor not as a seller of captured imagery but as a platform – one that uses its space segment to feed multiple SaaS-like products across commercial, enterprise, and defense markets, on a recurring-revenue base. Only that framing would support a ~$14.5 billion price tag. In multiple terms, that means roughly 7-8x revenue – about double the ~4x Vantor was bought at – or 15-20x EBITDA, a re-rating toward software comps.

That narrows the buyer universe to a few groups:

- Major legacy defense primes, or current leaders like Anduril and Palantir, looking for a stronger geospatial angle.

- Tech and AI players wanting a deeper USG inroad or a value-creation play on satellite data – Google being the obvious one, given the Earth AI relationship already in place, especially if they accept the spatial-AI narrative.

- An IPO: a return to public markets, again dependent on shareholders buying the recurring-revenue story or the defense-revenue growth case – and a more realistic path now that SpaceX's listing is priming public appetite for large space stocks

- Private equity, as a wild card – though most of the obvious value-creation levers have already been pulled, so a financial buyer would be betting on further EBITDA gains or on value beyond Legion and the software stack.

8. Closing Thoughts

In contrast to the Cobham playbook we discussed, divestments didn’t move the needle in this situation. The buyout structure mostly refinanced the debt during a difficult credit environment, with debt service acting as a constraint on the deal rather than a lever to juice equity returns. The room for multiple expansion is real, but it will come from Advent's active value creation across hardware, product, and positioning, not from an arbitrage sitting there to be claimed. And the customer concentration the whole thesis hinges on is the most likely thing to cap it.

The next 18-24 months will decide if this deal will become a success story or a cautionary tale. We will be closely watching for developments on a few fronts:

- Pulse (2027) and Vantage (2029) staying on schedule

- Vantor’s ability to monetize Legion as the most advanced commercial imaging system

- Whether Tensorglobe moves the company toward being a spatial intelligence platform with recurring revenue business, as opposed to just being a layer on top of imagery

- The EOCL contract extension to 2032 and any USG policy shift that disrupts the NRO-anchored revenue base.

With Maxar’s acquisition, Advent is playing the private equity game on the hardest settings. And we are curious to see the final score.

Sources

- Maxar 2022 10-K (last available): SEC

- Merger Plan (SEC): link

- BCI press release on close: link

- Advent close announcement: link

- Sixth Street Debt Facility (FT, gift): link

- Smoot - Crossing the Valley podcast: link

- Wilczynski - Crossing the Valley interview

- Smoot - LinkedIn post (~Jan 2026): link

- INTU press release on Lanteris: link

- INTU 13G (Advent stake): SEC

- Walter Scott "Why It Takes a Legion" - GeoIgnite keynote: video / coverage

- Geospatial World - Enterprise Spatial Intelligence: link

- S&P Global - PE holding periods: link

[1] A specific figure of 9.6% as an overall interest rate is mentioned here. While not a primary source, based on the conditions of previous loans and a benchmark for PE buyouts, we consider SOFR + 400-600 bp, yielding just under 10% as a reasonable assumption

[2] Lanteris held $622M cash at the time of Q3 earnings and the acquisition announcement, against 800 million total consideration for Lanteris.