Welcome to a belated, subscriber-exclusive, Pro edition of the TerraWatch newsletter. If you know someone who would benefit from this, please encourage them to subscribe so they can receive the newsletter every week.

If you want to receive the monthly deep-dives and get access to the archive, upgrade to a Premium subscription.

Quick housekeeping: We are hosting EO Summit next Monday, so there will no edition of this newsletter on June 22. We will be back the week after.

📈 EO Market Signals

💰 Deals & Funding

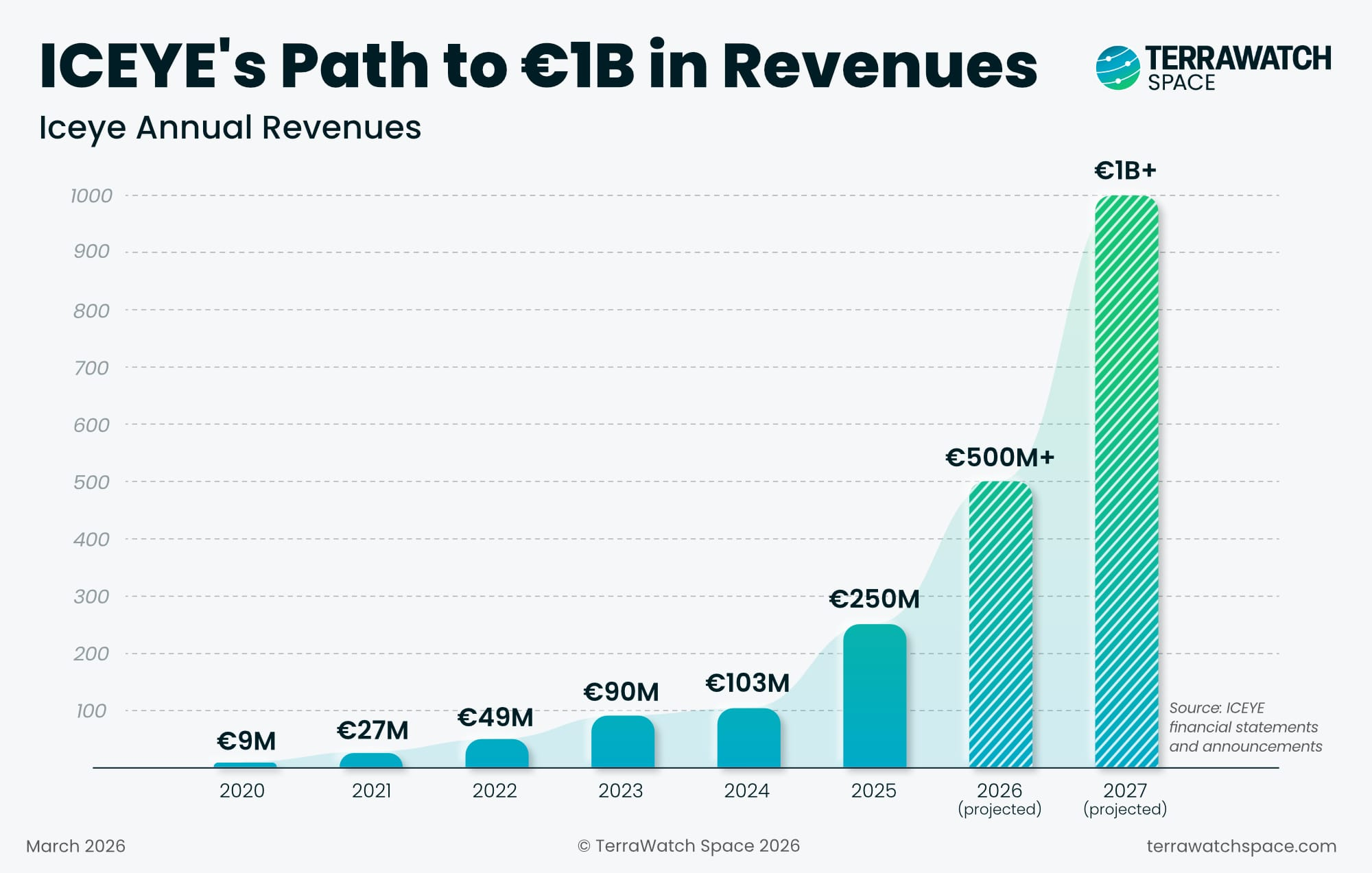

- ICEYE raised €450M in a Series F funding round at a valuation of over €10 billion. This, in addition to a secondary placement put the overall fundraising amount for this round to a whopping €1B. The company reported €250M in revenues in 2025, with over €100M in operating profits, and a contracted backlog of over €1.5B.

- ESA awarded a contract worth €700M to lead the development and build for two Copernicus Sentinel-1 Next Generation (NG) satellites to Thales Alenia Space, expected to launch in mid-2030s. Sentinel-1 NG will have improved capabilities of a wider swath (400 km vs current 250 km) and a higher resolution (5 x 5 m vs current 5 x 20 m).

As we see the commercial EO market evolving with increased resolution (up to 25 cm) and high-revisit, the civilian EO missions are also changing with the times.

- ESA awarded AAC Clyde Space a contract worth €10.9M to complete development of the Inflecion constellation that is built for maritime domain awareness combining SAR imagery and AIS/RF signals to detect vessels and communicate with them.

- Norwegian firm Kongsberg Satellite Services, together with a consortium, was awarded a €5M contract to build a maritime oil spill and environmental monitoring solution.

- BlackSky won a contract from the National Reconnaissance Office to accelerate the development of its AROS broad area collection satellites, the first of which will launch in 2028. These satellites are expected to enable a tip-and-cue workflow with their very high-resolution Gen-3 systems.

- Indian EO company SatSure received a grant of ₹24.6 crores (~$2.6M) from the state to develop Vision Foundation Models and Large Earth Observation Models purpose-built for India’s geographies, climate systems, and development priorities.

- NewOrbit Space, a UK startup developing satellites for very low Earth orbit has raised $18.5M in a Series A round, with plans to launch first satellites in 2028.

🎯 Moves & Strategy

- Airbus Defence and Space signed an agreement with thermal data provider constellr, electronics equipment manufacturer Rohde & Schwarz and other German startups to collaborate on a sovereign EO solution for Germany.

- German defense firm Rheinmetall and ICEYE announced the formation of a new joint venture Rheinmetall ICEYE Space Solutions that includes other German companies including Reflex Aerospace, OroraTech, constellr and LiveEO as partners.

Rheinmetall ICEYE Space Solutions, which won the €1.7B contract, is now with thermal (constellr, OroraTech), 3D imagery (LiveEO) and satellite platforms (Reflex). Airbus is positioning a competing MoU consortium with Rohde & Schwarz (SIGINT), constellr (thermal), Orbint (geolocation) and HPS (antennas).

One bloc has the win, while the other is positioning for the next contract. The startups straddling both such as constellr are sensibly hedging until the next decision lands.

🛰️ Other Signals

- Google open-sourced their hydrology model to enable National Meteorological and Hydrological Services to integrate advanced AI-based flood forecasting into their own workflows.

- Finnish weather data startup raised €6.5M to scale its atmospheric monitoring network that piggybacks on existing telecom infrastructure rather than deploying new hardware, in order to generate complementary measurements.

- Allen Institute for AI launched an EO-based AI agent to enable maritime analysts get answers for plain-language questions about what’s happening across the world’s oceans

- The Canadian Space Agency awarded three contracts, $804,000 each, to Calian, Kepler and MDA Space to develop concept studies for the ground segment of Canada's next-generation satellite system.

- An analysis found that Pakistan’s spy satellite network over India has grown faster than ever in 16 months.

- The Indian National Space Promotion and Authorisation agency has selected 15 projects to utilise EO to build solutions related to crop monitoring, flooding and disaster management use cases.

🔎 Featured Analysis

How ICEYE Became a Decacorn

When ICEYE sold two satellites to the Brazilian Air Force in 2020, the rest of the commercial EO was fixated on selling data and analytics as the only viable business model. Selling actual satellites to a national government was an outlier move that most of the EO industry treated as opportunistic.

Six years on, with ICEYE at a €10B valuation and a €1.5B contracted backlog, the Brazilian deal looks like early evidence of the thing ICEYE actually got right – a refusal to commit to one business model, and a willingness to sell customers whatever they were actually asking for: data to those who wanted data, analytics to those who wanted analytics, and satellites to those who wanted to own them.

ICEYE's didn't necessarily predict what was going to happen in the future with sovereign system, but they just had more flexibility in willingness to sell customers what they actually wanted (even when it broke the industry's preferred model at that time).

From Aalto University to the Largest SAR constellation

ICEYE began as a 2012 student project at Aalto University in Finland, when its CEO Rafał Modrzewski and its CSO Pekka Laurila were part of a joint Aalto-Stanford course exploring how to build satellites differently. By 2014 they had spun the work out as a company, built around a bet most of the industry thought was implausible. The thinking at that time was SAR satellites were bus-sized and typically built by national space agencies. But they hypothesised that SAR could be miniaturised to under 100 kg and operated as commercial constellations.

In January 2018, ICEYE launched ICEYE-X1, the first sub-100 kg commercial SAR satellite. The technical breakthrough was real, but the business model question was still open. The default assumption for commercial EO was the same as for optical: build a constellation, sell the data, layer analytics on top. ICEYE did all of that, and in parallel was already testing something else.

The 2020 Inflection

The Brazilian Air Force purchase, signed in December 2020 and launched in May 2022, was the first major test of selling satellites rather than just data. Other commercial EO operators, optical and SAR alike, had treated satellites as cost centres to be amortised across a long tail of data customers. ICEYE inverted the equation: a sovereign customer who wanted to own its piece of orbital infrastructure could pay a premium for the satellite itself, plus operations and capacity rights.

At the time, this was widely treated as a one-off. In hindsight, it was a strategic bet on a world that didn't yet exist — one in which national sovereignty over space-based intelligence would matter more than the marginal cost of data. That world through a number of geopolitical events arrived faster than anyone expected.

Defence and Geopolitics as the Growth Engine

The 2022 war in Ukraine surfaced what the Brazilian deal had only implied: commercial SAR was a sovereign capability that small and mid-sized nations could no longer leave to others. ICEYE's Ukraine engagement, via the Serhiy Prytula Charity Foundation, became the public proof of concept.

By 2025, the European sovereign procurement wave had already gotten mainstream. Poland, Netherlands, Finland, Portugal, and Sweden each signed sovereign SAR agreements with ICEYE, driven by Russia's threat and the growing uncertainty about the US as a partner. ICEYE's pitch by then was a deployable, taskable, nationally-controlled SAR capability with the option to put physical satellites under sovereign control.

The €1.7B contract with the German Bundeswehr, delivered through a joint venture with Rheinmetall, is the most consequential milestone of this trajectory. With satellite production in Germany and a defence industrial partner, ICEYE has crossed from being a commercial EO data vendor to a defence prime contractor. This was a transition that no other EO operator has made so far at this scale.

The revenue numbers (below) show the trajectory quite well: a €1.5B contracted backlog and €100M+ operating profits in 2025 confirm this is not a growth-at-all-costs story.

No commercial EO company has probably ever scaled like this, but then no new-age commercial EO company has ever been a defence prime contractor before either.

The Commercial Market Differentiation

Defence will dominate the topline for the rest of this decade, but ICEYE has been steadily building a commercial layer that matters for the longer arc. Its flood mapping and natural-catastrophe assessment products are now integrated into Munich Re, AXA, Aon and other major insurance carriers. In 2025, the company expanded into utilities and energy, providing SAR-derived damage assessment to grid operators during hurricanes and other extreme weather.

These verticals won't drive headline growth in the near term. What they do is build a recurring, subscription-like revenue base that will matter once defence procurement cycles eventually plateau. A decacorn-scale EO operator with both a sovereign defence book and an embedded commercial footprint in insurance and utilities is a structurally more durable business than pure-defence or pure-commercial alternatives.

So, What Did ICEYE Get Right?

Personally, I think ICEYE's real advantage was refusing to pick a single business model. While most EO operators committed to data-as-a-service and treated everything else as a distraction, ICEYE built the operational capability to sell data, analytics, and whole satellites — and let customers choose. The willingness to sell a satellite when a customer wanted to buy one, at a time when the rest of the industry insisted the customer should just license data was interesting.

And, that flexibility paid off. When the geopolitical environment shifted and nations started demanding sovereign systems, ICEYE didn't need to pivot. It was already doing the thing everyone now wants to do. By 2026, almost every major EO company is trying to build the same multi-model playbook. ICEYE has a head start in years, because it was selling satellites, data, and analytics in parallel while the rest of the industry was still arguing about which one was the real business.

A €10B valuation is not a stretch when the business model is satellites at a premium to countries who want their own, plus a commercial moat which is already operational with the world's largest insurance and finance companies. Given the contracted backlog, I don't think it is even aggressive (like the discussions of SpaceX's IPO has been). I think the valuation reflects a simple fact: ICEYE built a company the rest of the EO industry now wishes it had.

Until next time,

Aravind.